Model Optimization and Nonlinear Models#

CSC/DSC 340 Week 5 Slides

Author: Dr. Julie Butler

Date Created: August 19, 2023

Last Modified: September 18, 2023

Plan for the Week#

Monday

Week 5 Pre-Class Homework and Week 4 In-Class Assignment Due

Lecture: Model Optimization and Nonlinear Models

Office Hours: 1pm - 3pm

Tuesday

Office Hours: 4pm - 6pm

Wednesday

Finish Lecture: Model Optimization and Nonlinear Models

Start Week 5 In-Class Assignment

Week 4 Post-Class Homework Due

Thursday

Office Hours: 12:30 - 2pm

Friday

In-Class Assignment Week 5

Problem Analysis Due Before Class (~1 page)

Part 1: Hyperparameter Tuning#

Why do we need hyperparameter tuning?#

The values of the hyperparameters change the output of the model

Bad hyperparameters lead to bad results

##############################

## IMPORTS ##

##############################

import numpy as np

import matplotlib.pyplot as plt

from sklearn.linear_model import Lasso, Ridge

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_squared_error as MSE

from sklearn.datasets import fetch_california_housing

New data set: California Housing

Goal: Predict the price a house will sale for (house price/100k) given information about the house

In-Class Week 5

# Print the features

fetch_california_housing().feature_names

['MedInc',

'HouseAge',

'AveRooms',

'AveBedrms',

'Population',

'AveOccup',

'Latitude',

'Longitude']

##############################

## IMPORT DATA ##

##############################

X, y = fetch_california_housing(return_X_y = True)

##############################

## SCALE DATA ##

##############################

scaler = StandardScaler()

scaler.fit(X)

Z = scaler.transform(X)

##############################

## TRAIN-TEST SPLIT ##

##############################

X_train, X_test, y_train, y_test = train_test_split(Z,y,test_size=0.2)

##############################

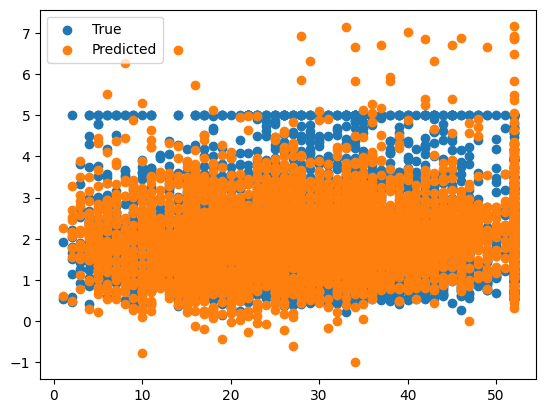

## GOOD ALPHA ##

##############################

ridge = Ridge(alpha=1e-15)

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

err = MSE(y_pred, y_test)

print("MSE:", err)

X_test_plot = scaler.inverse_transform(X_test)

plt.scatter(X_test_plot[:,1],y_test,label='True')

plt.scatter(X_test_plot[:,1],y_pred,label='Predicted')

plt.legend()

MSE: 0.5207853811806975

<matplotlib.legend.Legend at 0x1379a6610>

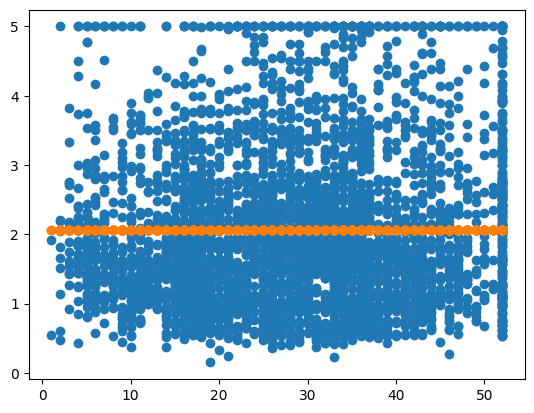

##############################

## BAD ALPHA ##

##############################

ridge = Ridge(alpha=1e15)

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

err = MSE(y_pred, y_test)

print("MSE:", err)

X_test_plot = scaler.inverse_transform(X_test)

plt.scatter(X_test_plot[:,1],y_test,label='True')

plt.scatter(X_test_plot[:,1],y_pred,label='Predicted')

MSE: 1.3166823615106975

<matplotlib.collections.PathCollection at 0x137a58970>

Methods for Hyperparameter Tuning#

Using Default Values#

Scikit-Learn sets the default value of \(\alpha\) for ridge regression to 1.0, which is a reasonable high level of regularization

# Make the data set smaller (20k+ points in total)

# More points = more data to generate patterns BUT more run time

X = X[:1000]

y = y[:1000]

X_train, X_test, y_train, y_test = train_test_split(X,y,test_size=0.2)

%%time

ridge = Ridge()

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

CPU times: user 2.43 ms, sys: 5.11 ms, total: 7.54 ms

Wall time: 1.29 ms

err = MSE(y_pred, y_test)

print("MSE:", err)

X_test_plot = scaler.inverse_transform(X_test)

plt.scatter(X_test_plot[:,1],y_test,label='True')

plt.scatter(X_test_plot[:,1],y_pred,label='Predicted')

MSE: 0.3596000507155571

<matplotlib.collections.PathCollection at 0x137b13cd0>

Pros#

Fast and no need to modify the algorithm

Cons#

Default value may not be the best value, but no test are done to check

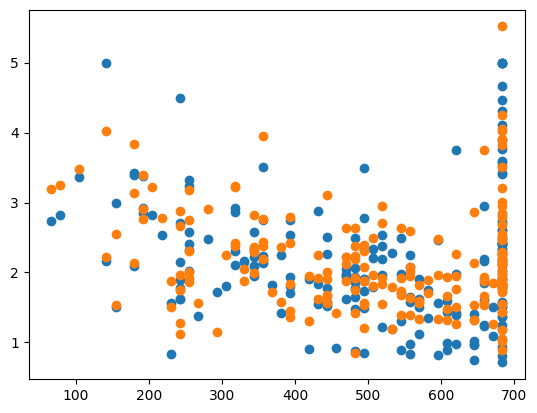

For Loop Tuning#

Use a for loop to check many different values for the hyperparameters

Can use nested for loops if more than one hyperparamter

%%time

best_err = 1e4

best_alpha = None

for alpha in np.logspace(-15,4,1000):

ridge = Ridge(alpha=alpha)

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

err = MSE(y_pred, y_test)

if err < best_err:

best_err = err

best_alpha = alpha

CPU times: user 630 ms, sys: 5.05 ms, total: 635 ms

Wall time: 297 ms

ridge = Ridge(alpha=best_alpha)

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

err = MSE(y_pred, y_test)

print("MSE:", err)

print("CHOSEN ALPHA:", best_alpha)

X_test_plot = scaler.inverse_transform(X_test)

plt.scatter(X_test_plot[:,1],y_test,label='True')

plt.scatter(X_test_plot[:,1],y_pred,label='Predicted')

MSE: 0.3552471269777846

CHOSEN ALPHA: 6.022541201461928e-15

<matplotlib.collections.PathCollection at 0x1076fbb50>

Pros#

Checks more than one value to find the best value

Simple concept

Short(ish) run times

Cons#

Long piece of code

Not checking all possible values of the hyperparameters

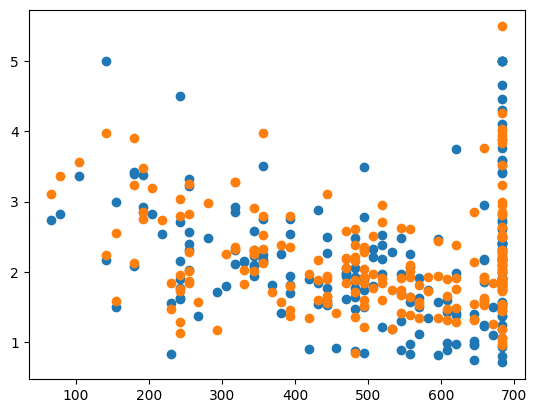

GridSearchCV (Scikit-Learn)#

Scikit-Learn has several hyperparameter tuning implementation

Grid search is a brute force algorithm which checks as many values as given

If more than one hyperparameter, it checks every single possible combination

“Same” test as for loops but gives much more information, but also takes longer

%%time

from sklearn.model_selection import GridSearchCV

parameters = {'alpha':np.logspace(-15,4,5000)}

ridge = Ridge()

grid_search = GridSearchCV(ridge, parameters,\

scoring='neg_mean_squared_error')

grid_search.fit(X_train, y_train)

print(grid_search.best_params_)

{'alpha': 0.20590302760544998}

CPU times: user 13.2 s, sys: 212 ms, total: 13.4 s

Wall time: 13.1 s

ridge = Ridge(alpha=grid_search.best_params_['alpha'])

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

err = MSE(y_pred, y_test)

print("MSE:", err)

print('CHOSEN ALPHA:', grid_search.best_params_['alpha'])

X_test_plot = scaler.inverse_transform(X_test)

plt.scatter(X_test_plot[:,1],y_test,label='True')

plt.scatter(X_test_plot[:,1],y_pred,label='Predicted')

MSE: 0.3562628152996591

CHOSEN ALPHA: 0.20590302760544998

<matplotlib.collections.PathCollection at 0x137e80a90>

Pros#

Only takes a few lines to implement

Gives a lot of data once it is fit

Cons#

Long run times

Only searches the range of parameters given

RandomizedSearchCV (Scikit-Learn)#

Tries

n_iterrandomly chosen values for the hyperparmeters taken from a given distribution (uniform in this case)

%%time

from sklearn.model_selection import RandomizedSearchCV

from scipy.stats import uniform

distributions = {'alpha':uniform(loc=0, scale=4)}

ridge = Ridge()

random_search = RandomizedSearchCV(ridge, distributions,\

scoring='neg_mean_squared_error', n_iter=5000)

random_search.fit(X_train, y_train)

print(random_search.best_params_, random_search.best_score_)

{'alpha': 0.20597888239758078} -0.28856463563603973

CPU times: user 13.3 s, sys: 230 ms, total: 13.5 s

Wall time: 13.2 s

ridge = Ridge(alpha=random_search.best_params_['alpha'])

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

err = MSE(y_pred, y_test)

print("MSE:", err)

print('CHOSEN ALPHA:', random_search.best_params_['alpha'])

X_test_plot = scaler.inverse_transform(X_test)

plt.scatter(X_test_plot[:,1],y_test,label='True')

plt.scatter(X_test_plot[:,1],y_pred,label='Predicted')

MSE: 0.35626318516764216

CHOSEN ALPHA: 0.20597888239758078

<matplotlib.collections.PathCollection at 0x164bb3940>

Pros#

Only takes a few lines to implement

Gives a lot of data once it is fit

Cons#

Long run times (depending on value of

n_iter)Only searches a finite number of parameter combinations

Bayesian Ridge Regression#

Finds the “most likely” value for \(\alpha\) using Bayesian stastics

Leaves no uncertainity that the best value was just not sampled

%%time

from sklearn.linear_model import BayesianRidge

bayesian_ridge = BayesianRidge()

bayesian_ridge.fit(X_train, y_train)

y_pred = bayesian_ridge.predict(X_test)

print(bayesian_ridge.alpha_)

3.688440522864384

CPU times: user 5.58 ms, sys: 1.28 ms, total: 6.85 ms

Wall time: 1.68 ms

ridge = BayesianRidge()

ridge.fit(X_train, y_train)

y_pred = ridge.predict(X_test)

err = MSE(y_pred, y_test)

print("MSE:", err)

print('CHOSEN ALPHA:', ridge.alpha_)

X_test_plot = scaler.inverse_transform(X_test)

plt.scatter(X_test_plot[:,1],y_test,label='True')

plt.scatter(X_test_plot[:,1],y_pred,label='Predicted')

MSE: 0.3592175812997633

CHOSEN ALPHA: 3.688440522864384

<matplotlib.collections.PathCollection at 0x164d18610>

Pros#

Only takes a few lines to implement

Statical certainity that the given \(\alpha\) value is the best value

Short run times

Cons#

Only valid for Bayesian ridge regression (linear model)

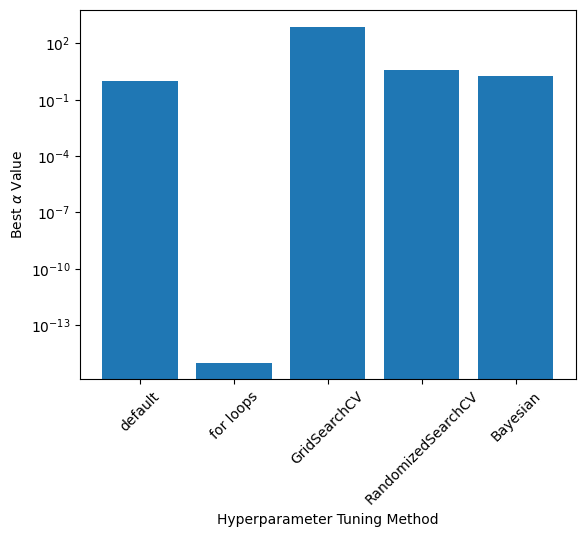

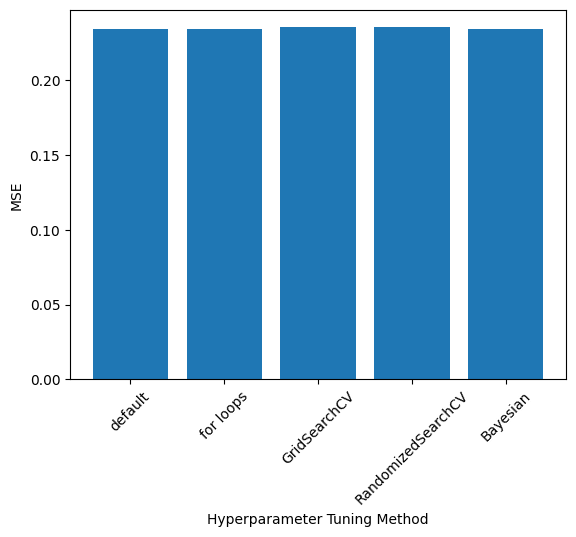

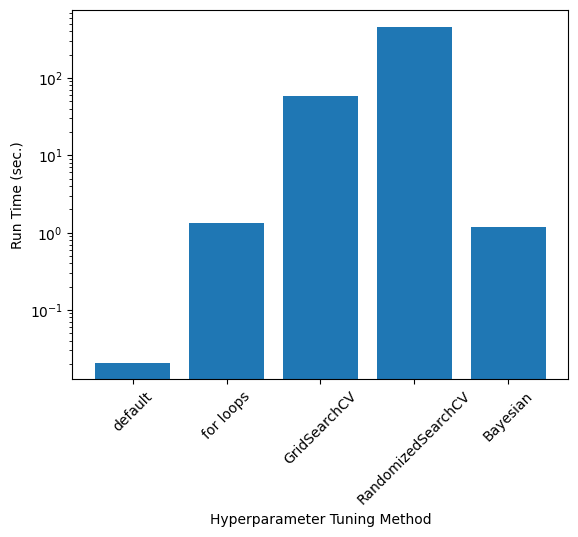

Comparison of \(\alpha\), Accuracy, and Run Time#

Exact values depend on the train-test split and RandomizedSearch results; these values were taken from one run

labels = ['default', 'for loops', 'GridSearchCV', 'RandomizedSearchCV', 'Bayesian']

alphas = [1.0, 1e-15, 769.79, 3.99, 1.90]

mse = [0.23461613368850237, 0.2343672966024232, 0.23546465060931623, 0.23546192678932165, 0.23439940455100014]

run_times = [20.8/1000, 1.35, 57.7, 7*60+40, 1.18] #ms

plt.bar(np.arange(0,len(labels)), alphas)

plt.yscale('log')

plt.xticks(np.arange(0,len(labels)), labels, rotation=45)

plt.ylabel(r"Best $\alpha$ Value")

plt.xlabel("Hyperparameter Tuning Method")

Text(0.5, 0, 'Hyperparameter Tuning Method')

plt.bar(np.arange(0,len(labels)), mse)

plt.xticks(np.arange(0,len(labels)), labels, rotation=45)

plt.ylabel(r"MSE")

plt.xlabel("Hyperparameter Tuning Method")

Text(0.5, 0, 'Hyperparameter Tuning Method')

plt.bar(np.arange(0,len(labels)), run_times)

plt.xticks(np.arange(0,len(labels)), labels, rotation=45)

plt.ylabel(r"Run Time (sec.)")

plt.xlabel("Hyperparameter Tuning Method")

plt.yscale('log')

Part 2: Feature Engineering#

Feature engineering is the process of eliminating or altering given inputs in order to improve the model’s predictions

Design matrix/alter the inputs

Remove features that are not useful

Scaling the features or targets

import pandas as pd

import seaborn as sns

housing = fetch_california_housing()

housing_data = pd.DataFrame(housing.data, columns=housing.feature_names)

housing_data['target'] = housing.target

housing_data = housing_data.sample(1000)

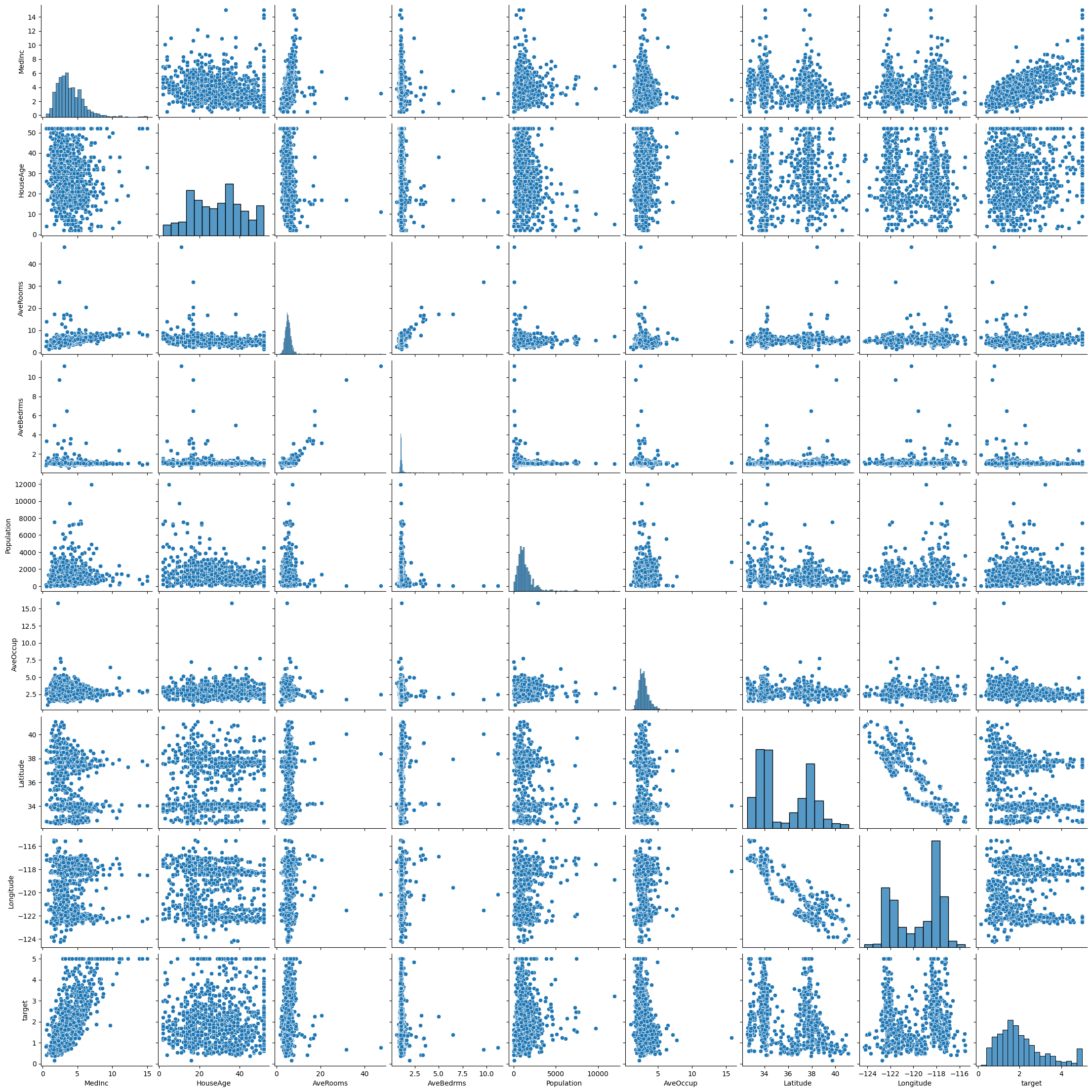

Pairplots can give us initial ideas about the data set and and obvious relations

sns.pairplot(housing_data)

/Users/juliehartley/Library/Python/3.9/lib/python/site-packages/seaborn/axisgrid.py:118: UserWarning: The figure layout has changed to tight

self._figure.tight_layout(*args, **kwargs)

<seaborn.axisgrid.PairGrid at 0x164247e20>

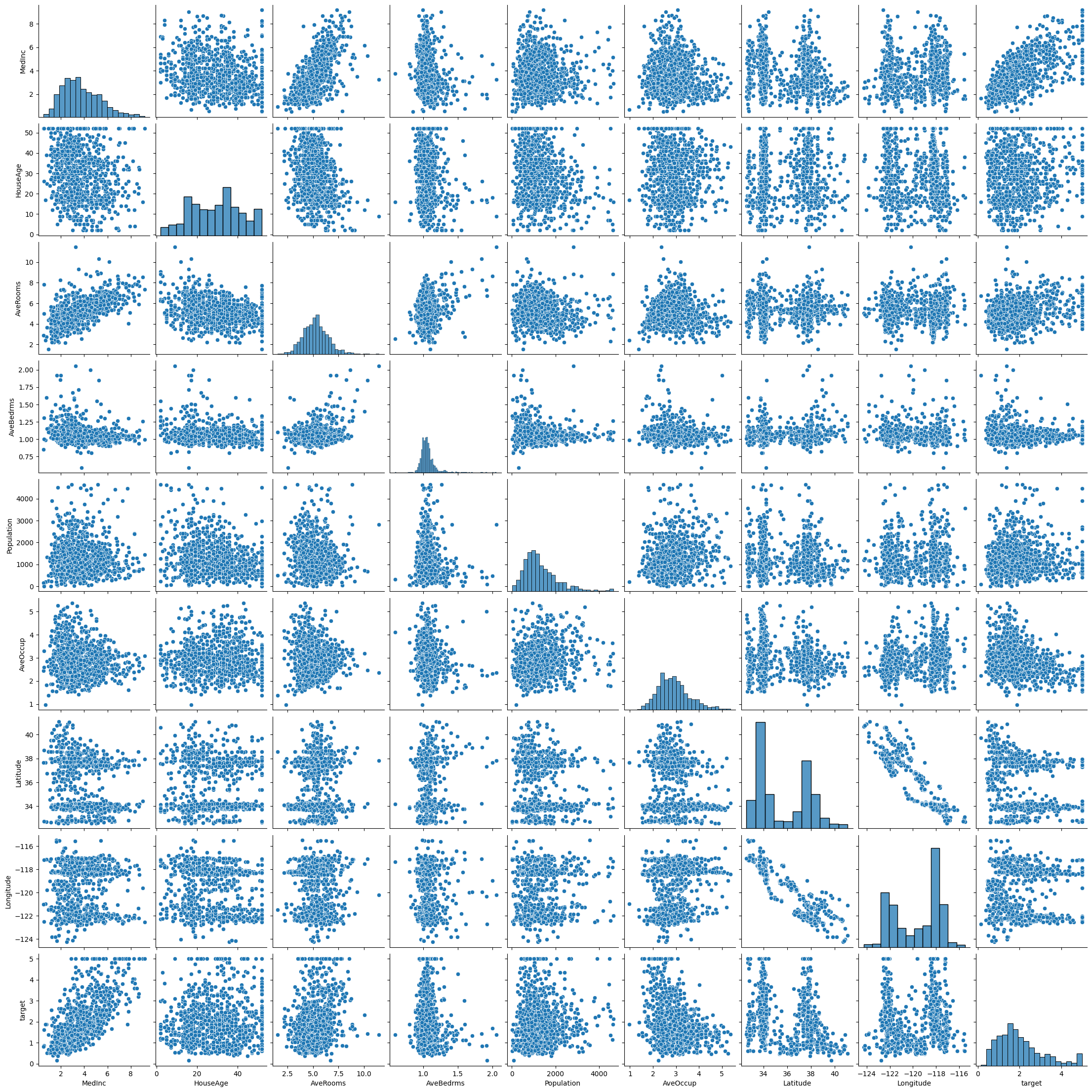

# Remove outliers from the data set and make the pairplot again

from scipy import stats

housing_data = housing_data[(np.abs(stats.zscore(housing_data)) < 3).all(axis=1)]

sns.pairplot(housing_data)

/Users/juliehartley/Library/Python/3.9/lib/python/site-packages/seaborn/axisgrid.py:118: UserWarning: The figure layout has changed to tight

self._figure.tight_layout(*args, **kwargs)

<seaborn.axisgrid.PairGrid at 0x1689a4070>

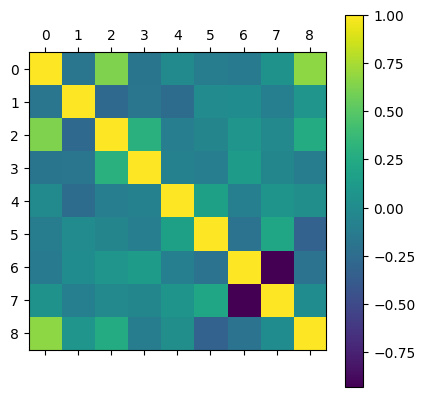

Correlation Matrix#

Correlation score = \(\sqrt{R2\ Score}\)

Values close to \(\pm1\) means that the two feautures are linearly related

correlation_matrix = housing_data.corr()

correlation_matrix

| MedInc | HouseAge | AveRooms | AveBedrms | Population | AveOccup | Latitude | Longitude | target | |

|---|---|---|---|---|---|---|---|---|---|

| MedInc | 1.000000 | -0.176376 | 0.624278 | -0.182821 | -0.006504 | -0.118286 | -0.145364 | 0.051990 | 0.671977 |

| HouseAge | -0.176376 | 1.000000 | -0.273970 | -0.171407 | -0.250648 | -0.000109 | 0.007118 | -0.100684 | 0.077059 |

| AveRooms | 0.624278 | -0.273970 | 1.000000 | 0.292713 | -0.108061 | -0.049828 | 0.077900 | -0.022613 | 0.254047 |

| AveBedrms | -0.182821 | -0.171407 | 0.292713 | 1.000000 | -0.080388 | -0.102396 | 0.132675 | -0.047917 | -0.121542 |

| Population | -0.006504 | -0.250648 | -0.108061 | -0.080388 | 1.000000 | 0.170063 | -0.097118 | 0.070431 | 0.019527 |

| AveOccup | -0.118286 | -0.000109 | -0.049828 | -0.102396 | 0.170063 | 1.000000 | -0.198600 | 0.214724 | -0.324090 |

| Latitude | -0.145364 | 0.007118 | 0.077900 | 0.132675 | -0.097118 | -0.198600 | 1.000000 | -0.931286 | -0.198935 |

| Longitude | 0.051990 | -0.100684 | -0.022613 | -0.047917 | 0.070431 | 0.214724 | -0.931286 | 1.000000 | 0.006876 |

| target | 0.671977 | 0.077059 | 0.254047 | -0.121542 | 0.019527 | -0.324090 | -0.198935 | 0.006876 | 1.000000 |

plt.matshow(correlation_matrix)

plt.colorbar()

<matplotlib.colorbar.Colorbar at 0x28b885fd0>

LASSO Regression for Feature Selection#

lasso = Lasso()

lasso.fit(X,y)

ypred = lasso.predict(X)

print(MSE(ypred,y))

lasso.coef_

0.638471842835069

array([ 0.06161184, -0. , 0. , -0. , 0.00011673,

-0. , 0. , 0. ])

Accuracy with All Data (Scaled)#

X = housing_data.drop(columns=['target'])

y = housing_data['target']

scaler = StandardScaler()

scaler.fit(X)

Z = scaler.transform(X)

X_train, X_test, y_train, y_test = train_test_split(Z,y,test_size=0.2)

bayesian_ridge = BayesianRidge()

bayesian_ridge.fit(X_train, y_train)

y_pred = bayesian_ridge.predict(X_test)

print('MSE:', MSE(y_pred, y_test))

MSE: 0.44933334607255193

Part 3: Nonlinear Models#

Kernel Ridge Regression (KRR)#

All previous models we have studied have been linear–capable of modeling linear patterns

Design matrices can only add some much functions

Many data sets will have a nonlinear pattern and thus we need a nonlinear model

Kernel ridge regression (KRR)

Support vector machines (SVMs)

Neural Networks

Kernel Functions#

Scikit-Learn kernels are found here

Linear: \(k(x,y) = x^Ty\)

Polynomial: k(x,y) = \((\gamma x^Ty+c_0)^d\)

Sigmoid: \(k(x,y) = tanh(\gamma x^Ty+c_0)\)

Radial Basis Function (RBF): \(k(x,y) = exp(-\gamma||x-y||_2)\)

Inputs to KRR algorithm are modified by the kernel function, thus giving the method nonlinearuty \(\longrightarrow\) kernel methods/trick allows linear methods to solve nonlinear problems

Kernel ridge regression is just ridge regression with the inputs modified by the kernel function

KRR Equations#

Form of predictions: \(\hat{y}(x) = \sum_{i=1}^m \theta_ik(x_i,x)\)

Loss function:\(J(\theta) = MSE(y,\hat{y}) + \frac{\alpha}{2}\sum_{i=1}^n\theta_i^2\)

Optimized parameters: \(\theta = (\textbf{K}-\alpha\textbf{I})^{-1}y\)

\(\textbf{K} = k(x_i, x_j)\)

Hyperparameter Tuning with Many Hyperparameters#

KRR has the same hyperparameter as ridge regression: \(\alpha\)

Each kernel function has 0-3 hyperparameters

The choice of kernel function is a hyperparameter

Hyperparameter tuning becomes more important as the number of hyperparameters in the model increases

Housing Data with Kernel Ridge Regression#

from sklearn.kernel_ridge import KernelRidge

X,y = fetch_california_housing(return_X_y=True)

X = X[:500]

y = y[:500]

scaler = StandardScaler()

scaler.fit(X)

Z = scaler.transform(X)

X_train, X_test, y_train, y_test = train_test_split(Z,y,test_size=0.2)

krr = KernelRidge()

krr.fit(X_train, y_train)

y_pred = krr.predict(X_test)

print("MSE:", MSE(y_pred, y_test))

MSE: 4.105741823609707

distributions = {'alpha':uniform(loc=0, scale=4), 'kernel':['linear', \

'polynomial', 'rbf', \

'sigmoid', 'laplacian'], \

'gamma':uniform(loc=0, scale=4),\

'degree':np.arange(0,10), 'coef0':uniform(loc=0, scale=4)}

krr = KernelRidge()

random_search = RandomizedSearchCV(krr, distributions,\

scoring='neg_mean_squared_error', n_iter=50)

random_search.fit(X_train, y_train)

print(random_search)

print(random_search.best_params_, random_search.best_score_)

---------------------------------------------------------------------------

KeyboardInterrupt Traceback (most recent call last)

Cell In [32], line 11

7 krr = KernelRidge()

9 random_search = RandomizedSearchCV(krr, distributions,\

10 scoring='neg_mean_squared_error', n_iter=50)

---> 11 random_search.fit(X_train, y_train)

12 print(random_search)

13 print(random_search.best_params_, random_search.best_score_)

File ~/Library/Python/3.9/lib/python/site-packages/sklearn/model_selection/_search.py:875, in BaseSearchCV.fit(self, X, y, groups, **fit_params)

869 results = self._format_results(

870 all_candidate_params, n_splits, all_out, all_more_results

871 )

873 return results

--> 875 self._run_search(evaluate_candidates)

877 # multimetric is determined here because in the case of a callable

878 # self.scoring the return type is only known after calling

879 first_test_score = all_out[0]["test_scores"]

File ~/Library/Python/3.9/lib/python/site-packages/sklearn/model_selection/_search.py:1753, in RandomizedSearchCV._run_search(self, evaluate_candidates)

1751 def _run_search(self, evaluate_candidates):

1752 """Search n_iter candidates from param_distributions"""

-> 1753 evaluate_candidates(

1754 ParameterSampler(

1755 self.param_distributions, self.n_iter, random_state=self.random_state

1756 )

1757 )

File ~/Library/Python/3.9/lib/python/site-packages/sklearn/model_selection/_search.py:822, in BaseSearchCV.fit.<locals>.evaluate_candidates(candidate_params, cv, more_results)

814 if self.verbose > 0:

815 print(

816 "Fitting {0} folds for each of {1} candidates,"

817 " totalling {2} fits".format(

818 n_splits, n_candidates, n_candidates * n_splits

819 )

820 )

--> 822 out = parallel(

823 delayed(_fit_and_score)(

824 clone(base_estimator),

825 X,

826 y,

827 train=train,

828 test=test,

829 parameters=parameters,

830 split_progress=(split_idx, n_splits),

831 candidate_progress=(cand_idx, n_candidates),

832 **fit_and_score_kwargs,

833 )

834 for (cand_idx, parameters), (split_idx, (train, test)) in product(

835 enumerate(candidate_params), enumerate(cv.split(X, y, groups))

836 )

837 )

839 if len(out) < 1:

840 raise ValueError(

841 "No fits were performed. "

842 "Was the CV iterator empty? "

843 "Were there no candidates?"

844 )

File ~/Library/Python/3.9/lib/python/site-packages/joblib/parallel.py:1088, in Parallel.__call__(self, iterable)

1085 if self.dispatch_one_batch(iterator):

1086 self._iterating = self._original_iterator is not None

-> 1088 while self.dispatch_one_batch(iterator):

1089 pass

1091 if pre_dispatch == "all" or n_jobs == 1:

1092 # The iterable was consumed all at once by the above for loop.

1093 # No need to wait for async callbacks to trigger to

1094 # consumption.

File ~/Library/Python/3.9/lib/python/site-packages/joblib/parallel.py:901, in Parallel.dispatch_one_batch(self, iterator)

899 return False

900 else:

--> 901 self._dispatch(tasks)

902 return True

File ~/Library/Python/3.9/lib/python/site-packages/joblib/parallel.py:819, in Parallel._dispatch(self, batch)

817 with self._lock:

818 job_idx = len(self._jobs)

--> 819 job = self._backend.apply_async(batch, callback=cb)

820 # A job can complete so quickly than its callback is

821 # called before we get here, causing self._jobs to

822 # grow. To ensure correct results ordering, .insert is

823 # used (rather than .append) in the following line

824 self._jobs.insert(job_idx, job)

File ~/Library/Python/3.9/lib/python/site-packages/joblib/_parallel_backends.py:208, in SequentialBackend.apply_async(self, func, callback)

206 def apply_async(self, func, callback=None):

207 """Schedule a func to be run"""

--> 208 result = ImmediateResult(func)

209 if callback:

210 callback(result)

File ~/Library/Python/3.9/lib/python/site-packages/joblib/_parallel_backends.py:597, in ImmediateResult.__init__(self, batch)

594 def __init__(self, batch):

595 # Don't delay the application, to avoid keeping the input

596 # arguments in memory

--> 597 self.results = batch()

File ~/Library/Python/3.9/lib/python/site-packages/joblib/parallel.py:288, in BatchedCalls.__call__(self)

284 def __call__(self):

285 # Set the default nested backend to self._backend but do not set the

286 # change the default number of processes to -1

287 with parallel_backend(self._backend, n_jobs=self._n_jobs):

--> 288 return [func(*args, **kwargs)

289 for func, args, kwargs in self.items]

File ~/Library/Python/3.9/lib/python/site-packages/joblib/parallel.py:288, in <listcomp>(.0)

284 def __call__(self):

285 # Set the default nested backend to self._backend but do not set the

286 # change the default number of processes to -1

287 with parallel_backend(self._backend, n_jobs=self._n_jobs):

--> 288 return [func(*args, **kwargs)

289 for func, args, kwargs in self.items]

File ~/Library/Python/3.9/lib/python/site-packages/sklearn/utils/fixes.py:117, in _FuncWrapper.__call__(self, *args, **kwargs)

115 def __call__(self, *args, **kwargs):

116 with config_context(**self.config):

--> 117 return self.function(*args, **kwargs)

File ~/Library/Python/3.9/lib/python/site-packages/sklearn/model_selection/_validation.py:686, in _fit_and_score(estimator, X, y, scorer, train, test, verbose, parameters, fit_params, return_train_score, return_parameters, return_n_test_samples, return_times, return_estimator, split_progress, candidate_progress, error_score)

684 estimator.fit(X_train, **fit_params)

685 else:

--> 686 estimator.fit(X_train, y_train, **fit_params)

688 except Exception:

689 # Note fit time as time until error

690 fit_time = time.time() - start_time

File ~/Library/Python/3.9/lib/python/site-packages/sklearn/kernel_ridge.py:195, in KernelRidge.fit(self, X, y, sample_weight)

192 ravel = True

194 copy = self.kernel == "precomputed"

--> 195 self.dual_coef_ = _solve_cholesky_kernel(K, y, alpha, sample_weight, copy)

196 if ravel:

197 self.dual_coef_ = self.dual_coef_.ravel()

File ~/Library/Python/3.9/lib/python/site-packages/sklearn/linear_model/_ridge.py:249, in _solve_cholesky_kernel(K, y, alpha, sample_weight, copy)

243 K.flat[:: n_samples + 1] += alpha[0]

245 try:

246 # Note: we must use overwrite_a=False in order to be able to

247 # use the fall-back solution below in case a LinAlgError

248 # is raised

--> 249 dual_coef = linalg.solve(K, y, assume_a="pos", overwrite_a=False)

250 except np.linalg.LinAlgError:

251 warnings.warn(

252 "Singular matrix in solving dual problem. Using "

253 "least-squares solution instead."

254 )

File ~/Library/Python/3.9/lib/python/site-packages/scipy/linalg/_basic.py:251, in solve(a, b, lower, overwrite_a, overwrite_b, check_finite, assume_a, transposed)

247 # Positive definite case 'posv'

248 else:

249 pocon, posv = get_lapack_funcs(('pocon', 'posv'),

250 (a1, b1))

--> 251 lu, x, info = posv(a1, b1, lower=lower,

252 overwrite_a=overwrite_a,

253 overwrite_b=overwrite_b)

254 _solve_check(n, info)

255 rcond, info = pocon(lu, anorm)

KeyboardInterrupt:

X,y = fetch_california_housing(return_X_y=True)

scaler = StandardScaler()

scaler.fit(X)

Z = scaler.transform(X)

X_train, X_test, y_train, y_test = train_test_split(Z,y,test_size=0.2)

# Using the best parameters from through one run of the

# RandomizedSearchCV method above

krr = KernelRidge(alpha= 0.35753693232459094, coef0= 3.2725118241858264, degree= 9, gamma= 0.14696609545731532, kernel= 'laplacian')

krr.fit(X_train, y_train)

y_pred = krr.predict(X_test)

print('MSE:', MSE(y_pred, y_test))

MSE: 0.23499324697787755

bayesian_ridge = BayesianRidge()

bayesian_ridge.fit(X_train, y_train)

y_pred = bayesian_ridge.predict(X_test)

print('MSE:', MSE(y_pred, y_test))

MSE: 0.5242651488478602